All Categories

Featured

Table of Contents

- – How can Policy Loans reduce my reliance on ban...

- – What financial goals can I achieve with Infini...

- – How do I track my growth with Whole Life For ...

- – Can I access my money easily with Infinite Ba...

- – What are the most successful uses of Infinit...

- – What financial goals can I achieve with Poli...

- – Is Cash Flow Banking a better option than sa...

Term life is the excellent service to a short-lived demand for protecting versus the loss of an income producer. There are much fewer factors for permanent life insurance policy. Key-man insurance coverage and as component of a buy-sell contract entered your mind as a feasible good reason to buy a permanent life insurance policy plan.

It is an expensive term created to market high valued life insurance policy with adequate commissions to the agent and substantial earnings to the insurance coverage companies. Wealth building with Infinite Banking. You can get to the very same end result as unlimited financial with much better outcomes, even more liquidity, no threat of a policy lapse setting off an enormous tax trouble and more alternatives if you utilize my choices

How can Policy Loans reduce my reliance on banks?

Contrast that to the prejudices the promoters of infinity banking get. 5 Blunders People Make With Infinite Banking.

As you approach your golden years, economic safety is a leading priority. Among the many different economic strategies available, you might be listening to a growing number of regarding infinite banking. Infinite Banking. This principle allows practically anybody to become their very own bankers, offering some benefits and adaptability that can fit well into your retirement plan

What financial goals can I achieve with Infinite Banking Cash Flow?

The loan will accumulate simple interest, however you keep versatility in setting settlement terms. The rate of interest is additionally generally lower than what you would certainly pay a traditional bank. This sort of withdrawal permits you to access a portion of your cash worth (up to the quantity you've paid in costs) tax-free.

Many pre-retirees have problems regarding the safety and security of infinite banking, and completely factor. While it is a legitimate strategy that's been taken on by individuals and companies for many years, there are risks and downsides to take into consideration. Infinite financial is not a guaranteed means to build up wealth. The returns on the cash value of the insurance coverage policies might change relying on what the marketplace is doing.

How do I track my growth with Whole Life For Infinite Banking?

Infinite Banking is a financial strategy that has actually gotten considerable attention over the previous few years. It's an one-of-a-kind approach to handling individual financial resources, allowing people to take control of their cash and produce a self-sustaining banking system - Tax-free income with Infinite Banking. Infinite Banking, also called the Infinite Financial Concept (IBC) or the Count on Yourself approach, is a financial technique that entails using dividend-paying entire life insurance coverage policies to produce a personal banking system

Life insurance is an essential part of financial planning that provides numerous advantages. Borrowing against cash value. It comes in many shapes and sizes, the most typical types being term life, entire life, and global life insurance policy.

Can I access my money easily with Infinite Banking Cash Flow?

Allow's discover what each kind is and just how they differ. Term life insurance policy, as its name suggests, covers a specific duration or term, normally in between 10 to thirty years. It is the simplest and frequently one of the most economical sort of life insurance policy. If the insurance policy holder passes away within the term, the insurance provider will certainly pay out the survivor benefit to the marked recipients.

Some term life policies can be renewed or exchanged a permanent policy at the end of the term, however the premiums typically raise upon renewal as a result of age. Whole life insurance policy is a kind of long-term life insurance policy that supplies protection for the insurance policy holder's entire life. Unlike term life insurance policy, it includes a cash money worth part that grows with time on a tax-deferred basis.

It's important to remember that any kind of impressive car loans taken against the plan will certainly reduce the death benefit. Whole life insurance coverage is normally more costly than term insurance since it lasts a life time and develops cash money value. It likewise offers predictable costs, meaning the price will not raise over time, providing a degree of assurance for insurance policy holders.

What are the most successful uses of Infinite Banking In Life Insurance?

Some factors for the misconceptions are: Complexity: Whole life insurance policies have extra elaborate functions contrasted to label life insurance, such as cash value build-up, rewards, and policy fundings. These functions can be challenging to comprehend for those without a background in insurance or personal money, causing confusion and mistaken beliefs.

Predisposition and false information: Some people might have had negative experiences with entire life insurance or heard tales from others that have. These experiences and anecdotal info can add to a biased view of whole life insurance policy and perpetuate misunderstandings. The Infinite Banking Principle approach can only be carried out and carried out with a dividend-paying whole life insurance policy plan with a common insurance policy business.

Whole life insurance policy is a kind of long-term life insurance that provides insurance coverage for the insured's whole life as long as the costs are paid. Entire life plans have two major parts: a death benefit and a money value (Life insurance loans). The death advantage is the quantity paid out to recipients upon the insured's fatality, while the money worth is a cost savings element that expands gradually

What financial goals can I achieve with Policy Loan Strategy?

Returns payments: Shared insurer are possessed by their insurance holders, and because of this, they might disperse revenues to insurance holders in the kind of rewards. While returns are not ensured, they can aid boost the cash money value development of your plan, increasing the total return on your funding. Tax benefits: The cash worth development within a whole life insurance policy plan is tax-deferred, indicating you do not pay taxes on the growth up until you take out the funds.

This can supply substantial tax benefits contrasted to other financial savings and financial investments. Liquidity: The cash money worth of an entire life insurance plan is very liquid, allowing you to gain access to funds quickly when needed. This can be especially useful in emergencies or unanticipated economic circumstances. Possession protection: In many states, the cash worth of a life insurance policy plan is protected from lenders and lawsuits.

Is Cash Flow Banking a better option than saving accounts?

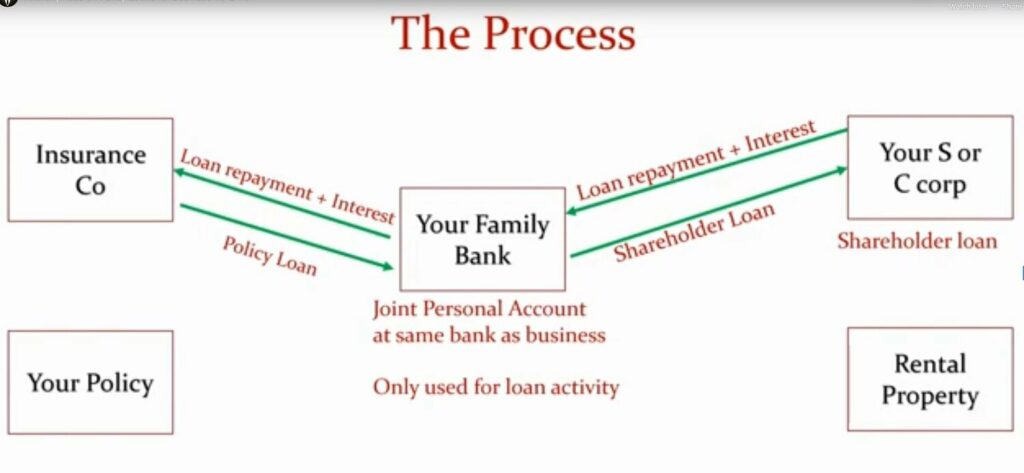

The policy will have immediate money value that can be placed as security 30 days after funding the life insurance coverage policy for a rotating line of credit history. You will have the ability to gain access to via the rotating credit line up to 95% of the available money worth and utilize the liquidity to money an investment that provides earnings (capital), tax benefits, the chance for appreciation and leverage of other individuals's capability, capacities, networks, and funding.

Infinite Financial has actually ended up being popular in the insurance world - a lot more so over the last 5 years. Many insurance agents, throughout social networks, case to do IBC. Did you know there is an? R. Nelson Nash was the designer of Infinite Financial and the organization he started, The Nelson Nash Institute, is the only company that officially licenses insurance policy agents as "," based upon the complying with criteria: They straighten with the NNI standards of professionalism and trust and ethics.

They effectively complete an instruction with a senior Licensed IBC Expert to guarantee their understanding and capacity to use every one of the above. StackedLife is Accredited IBC in the San Francisco Bay Location and functions nation-wide, helping clients comprehend and apply The IBC.

{kind=link}

Table of Contents

- – How can Policy Loans reduce my reliance on ban...

- – What financial goals can I achieve with Infini...

- – How do I track my growth with Whole Life For ...

- – Can I access my money easily with Infinite Ba...

- – What are the most successful uses of Infinit...

- – What financial goals can I achieve with Poli...

- – Is Cash Flow Banking a better option than sa...

Latest Posts

Infinite Life Insurance

Bank On Yourself: How To Become Your Own Bank

"Infinite Banking" Or "Be Your Own Bank" Via Whole Life ...

More

Latest Posts

Infinite Life Insurance

Bank On Yourself: How To Become Your Own Bank

"Infinite Banking" Or "Be Your Own Bank" Via Whole Life ...